Based on ATTOM’s newly released first-quarter 2023 U.S. Home Affordability Report, median-priced single-family homes and condos are less affordable in the first quarter of 2023 compared to historical averages in 94 percent of counties across the nation with enough data to analyze – far above the 62 percent of counties that were historically less affordable in the first quarter of 2022.

However, the report also shows that buying conditions for house hunters may be improving as the portion of average wages nationwide required for typical major home-ownership expenses has fallen slightly to 30 percent this quarter.

The latest percentage is still considered unaffordable by common lending standards, which call for a 28 percent debt- to-income ratio. It also remains well above the 25 percent level in the first quarter of 2022. But the portion has inched downward from 31 percent in the final months of last year.

The mixed picture facing home buyers – prices that remain a financial stretch but are getting a bit more affordable – reflects a softening of the U.S. housing market combined with rising wages at a time when home-mortgage rates have stabilized following a year of increases.

The nationwide median single-family home and condo price is up less than 1 percent from the fourth quarter of 2022 to the first quarter of 2023 – now sitting at $320,000 – while three quarters of local markets continue to see prices slip this year. Those trends have followed an 8 percent decrease in the nationwide median during the second half of 2022. The drop-off has come as rising interest rates, high consumer-price inflation and stock market declines have cut into what home seekers can afford or the resources they have for down payments.

At the same time, wages have risen 6 percent nationwide over the past year, with increases continuing into the second half of 2022 in most of the country.

“The soaring housing market has finally come back down in much of the U.S., at least for now, while worker pay is growing. That’s produced some benefits for home seekers in the form of slightly better affordability, especially as lending rates have flattened out,” said Rob Barber, chief executive office for ATTOM. “Things certainly haven’t swung way back into friendly territory. Price drops and wage gains haven’t yet translated into equal improvements in affordability. And the trend could go back the other way if interest rates go up again, as expected. But the scenario is becoming more favorable for buyers.”

With multiple uncertain economic forces at work, the market could continue sliding or turn back upward this Spring and Summer. That, along with the path of wages, will dictate whether home ownership continues to grow more affordable after a gradual path the other way over the past few years.

ATTOM’s report determined affordability for average wage earners by calculating the amount of income needed to meet major monthly home ownership expenses — including mortgage, property taxes and insurance — on a median-priced single-family home and condo, assuming a 20 percent down payment and a 28 percent maximum “front-end” debt-to-income ratio. That required income was then compared to annualized average weekly wage data from the Bureau of Labor Statistics.

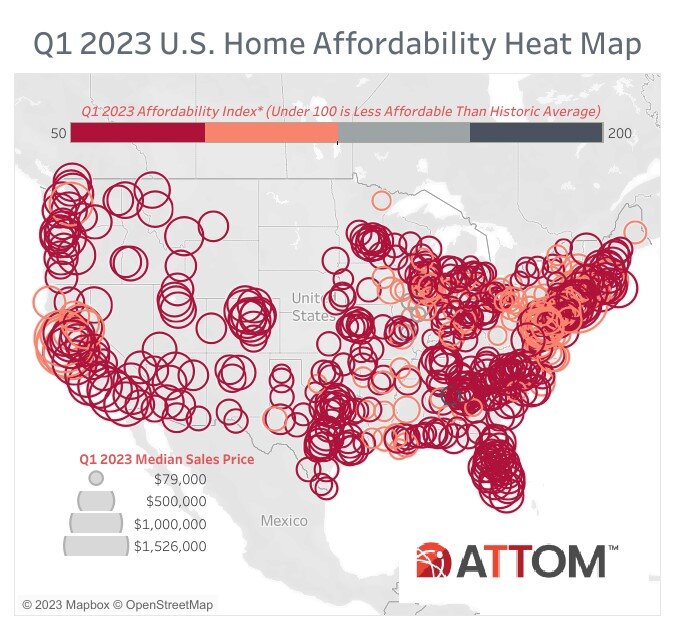

Compared to historical levels, median home prices in 537 of the 572 counties analyzed in the first quarter of 2023 are less affordable than in the past. The latest number is down from 565 of the same group of counties in the fourth quarter of 2022. But it remains far more than 356 in the first quarter of 2022 and just 91, or less than one-fifth, that were less affordable historically two years ago.

Meanwhile, major home-ownership expenses on typical homes are considered unaffordable to average local wage earners during the first quarter of 2023 in 373, or about two-thirds, of the 572 counties in the report, based on the 28 percent guideline. Counties with the largest populations that are unaffordable in the first quarter are Los Angeles County, CA; Maricopa County (Phoenix), AZ; San Diego County, CA; Orange County, CA (outside Los Angeles) and Kings County (Brooklyn), NY.

The most populous of the 199 counties where major expenses on median-priced homes remain affordable for average local workers in the first quarter of 2023 are Cook County (Chicago), IL; Harris County (Houston), TX; Wayne County (Detroit), MI; Philadelphia County, PA, and Franklin County (Columbus), OH.

Home prices up slightly nationwide, but down in three-quarters of local markets

The recent slowdown in the U.S. housing market after 10 years of increases has flattened the national median single-family home and condo value, while pushing prices down in most counties so far this year.

Nationwide, the median single-family home, and condo value of $320,000 in the first quarter of 2023 is virtually the same as the typical $318,000 price in the fourth quarter of 2022 and is up just 1.3 percent from $316,000 in the first quarter of last year.

At the local level, median home prices in the first quarter of 2023 remain up from the first quarter of last year in 371, or 65 percent, of those counties.

Data was analyzed for counties with a population of at least 100,000 and at least 50 single-family home and condo sales in the first quarter of 2023.

Among the 46 counties in the report with a population of at least 1 million, the biggest year-over-year increase in median sale prices during the first quarter of 2023 are in St. Louis County, MO (up 38 percent); Palm Beach County (West Palm Beach), FL (up 11 percent); Collin County (Plano), TX (up 10 percent); Franklin County (Columbus), OH (up 7 percent) and Miami-Dade County, FL (up 6 percent).

Counties with a population of at least 1 million where median prices have dropped most from the first quarter of 2022 to the same period this year are Alameda County (Oakland), CA (down 16 percent); Santa Clara County (San Jose), CA (down 12 percent); Contra Costa County, CA (outside San Francisco) (down 12 percent); Philadelphia County, PA (down 11 percent) and King County (Seattle), WA (down 8 percent).

Wages growing faster than prices in 76 percent of markets

Weekly annualized wage appreciation has outpaced annual home-price changes in the first quarter of 2023 in 433 of the 572 counties analyzed in the report (76 percent). That was the opposite of the first quarter of last year when prices were growing faster than wages in 87 percent of the same counties.

The current group where wage gains are outpacing price changes include Los Angeles County, CA; Cook County, (Chicago), IL; Harris County (Houston), TX; Maricopa County (Phoenix), AZ, and San Diego County, CA.

Year-over-year price gains have surpassed average annualized wage growth during the first quarter of 2023 in just 139 of the 572 counties analyzed (24 percent). The latest group where prices are going up faster than wages include Kings County (Brooklyn), NY; Franklin County (Columbus), OH; Collin County (Plano), TX; St. Louis County, MO, and Westchester County, NY (outside New York City).

Portion of wages needed for home ownership decreases throughout the U.S. even as lending benchmark is still exceeded in two-thirds of the nation

With 30-year mortgage rates leveling off this year after doubling in 2022, the portion of average local wages consumed by major expenses on median-priced, single-family homes and condos has decreased from the fourth quarter of 2022 to the first quarter of 2023 in 97 percent of the 572 counties analyzed.

The typical $1,758 cost of mortgage payments, homeowner insurance, mortgage insurance and property taxes nationwide now requires 29.9 percent of the average annual $70,460 wage. That is down from 31.2 percent in the fourth quarter of 2022 – the highest level in 15 years – although still up from 24.9 percent a year ago.

The latest portion still tops the 28 percent lending guideline in 373, or about three-quarters of those counties, assuming a 20 percent down payment. But that is down from 407, or almost three-quarters, of the same group of counties in the fourth quarter of 2022.

“The affordability gains we are seeing so far this year, small as they are, could start to lure buyers back into the markets where they were once put off by soaring prices,” Barber said. “That would help all segments of the market, especially high-end areas that suffered some of the larger price declines since the market started to stall last year.”

Counties with the largest quarterly decrease in the portion of average local wages needed for major ownership expenses are Marin County, CA (outside San Francisco) (down from 102 percent in the fourth quarter of 2022 to 87.8 percent in the first quarter of 2023); Washington County, UT (northeast of Las Vegas, NV) (down from 73.5 percent to 62.6 percent); Santa Cruz County, CA (down from 110.9 percent to 100.8 percent); Nevada County, CA (outside Reno, NV) (down from 71.5 percent to 61.7 percent) and Alameda County (Oakland), CA (down from 71.4 percent to 61.8 percent).

Homeownership consumes largest chunk of wages on east and west coasts

Counties where major ownership costs require the largest percentage of wages are concentrated on the east and west coasts, led by Kings County (Brooklyn), NY (110 percent of annualized local weekly wages needed to buy a single-family home); Santa Cruz County, CA (100.8 percent); Maui County, HI (96.4 percent); Monterey County, CA (88.3 percent) and Marin County, CA (outside San Francisco) (87.8 percent).

Aside from Kings County, NY, counties with a population of at least 1 million where major ownership expenses typically consume more than 28 percent of average local wages in the first quarter of 2023 include Orange County, CA (outside Los Angeles) (78.5 percent required); Queens County, NY (75.4 percent); Nassau County (Long Island), NY (65.4 percent) and Riverside County, CA (65.4 percent).

Counties where the smallest portion of average local wages are required to afford the median-priced home during the first quarter of this year are Macon County (Decatur), IL (9.9 percent of annualized weekly wages needed to buy a home); Peoria County, IL (10.4 percent); Schuylkill County, PA (outside Allentown) (11.1 percent); Rock Island County (Davenport), IL (12.3 percent) and Wayne County (Detroit), MI (12.7 percent).

Aside from Wayne County, MI, counties with a population of at least 1 million where major ownership expenses typically consume less than 28 percent of average local wages in the first quarter of 2023 include Philadelphia County, PA (16 percent); Cuyahoga County (Cleveland), OH (17 percent); Cook County (Chicago), IL (22.3 percent) and St. Louis County, MO (25.2 percent).

Annual wages of more than $75,000 needed to afford typical home in half of markets

Despite improving affordability, annual wages of more than $75,000 still are needed to pay for major costs on the median-priced home purchased during the first quarter of 2023 in 285, or 50 percent, of the 572 markets in the report.

The top 25 highest annual wages required to afford typical homes again are on the east or west coasts, led by New York County (Manhattan), NY ($393,132); San Mateo County (outside San Francisco), CA ($354,814); Marin County (outside San Francisco), CA ($328,712); San Francisco County, CA ($321,805) and Santa Clara County (San Jose), CA ($316,948).

The lowest annual wages required to afford a median-priced home in the first quarter of 2023 are in Schuylkill County, PA (outside Allentown) ($21,880); St. Lawrence County, NY (north of Syracuse) ($25,924); Macon County (Decatur), IL ($26,677); Fayette County, PA (south of Pittsburgh) ($27,631) and Bibb County (Macon), GA ($28,574).

Home affordability worse than historical averages in most of nation, but improving

Among the 572 counties analyzed, 537, or 94 percent, are less affordable in the first quarter of 2023 than their historic affordability averages. That is far higher than the 62 percent level of a year ago, but down from 99 percent in the fourth quarter of 2022. Historical indexes improved quarterly in 97 percent of those counties, helping to boost the nationwide index up from a 15-year low hit at the end of last year.

Counties with a population of at least 1 million that are less affordable than their historic averages (indexes of less than 100 are considered less affordable compared to historic averages) include Collin County (Plano), TX (index of 65); Tarrant County (Fort Worth), TX (66); Hillsborough County (Tampa), FL (67); Mecklenburg County (Charlotte), NC (69) and Dallas County, TX (69).

Counties with the worst affordability indexes in the first quarter of 2023 are Jackson County, MS (outside Mobile, AL) (index of 48); Clayton County, GA (outside Atlanta) (53); Benton County (Kennewick), WA (58); Paulding County, GA (outside Marietta) (58) and St. Lucie County (Port St. Lucie), FL (59).

Among counties with a population of at least 1 million, those were the affordability indexes have improved most from the fourth quarter of 2022 to the first quarter of 2023 are Wayne County (Detroit), MI (index up 21 percent); Alameda County (Oakland), CA (up 16 percent); Contra Costa County, CA (outside San Francisco) (up 14 percent); Philadelphia County, PA (up 14 percent) and Cuyahoga County (Cleveland), OH (up 13 percent).

Only 6 percent of markets are more affordable than historic averages

Among the 572 counties in the report, only 35 (6 percent) are more affordable than their historic averages in the first quarter of 2023. That is still well down from 38 percent a year ago but up from 1 percent in the fourth quarter of 2022.

Counties that are more affordable in the first quarter of this year compared to historical averages include Macon County (Decatur), IL Y(index of 158); Peoria County, IL (135); St. Clair County, IL (outside St. Louis, MO) (130); San Francisco County, CA (125) and Caddo Parish (Shreveport), LA (117).